When someone applies for a loan, banks don’t just take their word for it. They ask for supporting documents — simple proof that the borrower is who they say they are and can repay the money.

Here’s why these documents matter and what they usually include.

Proof of Identity

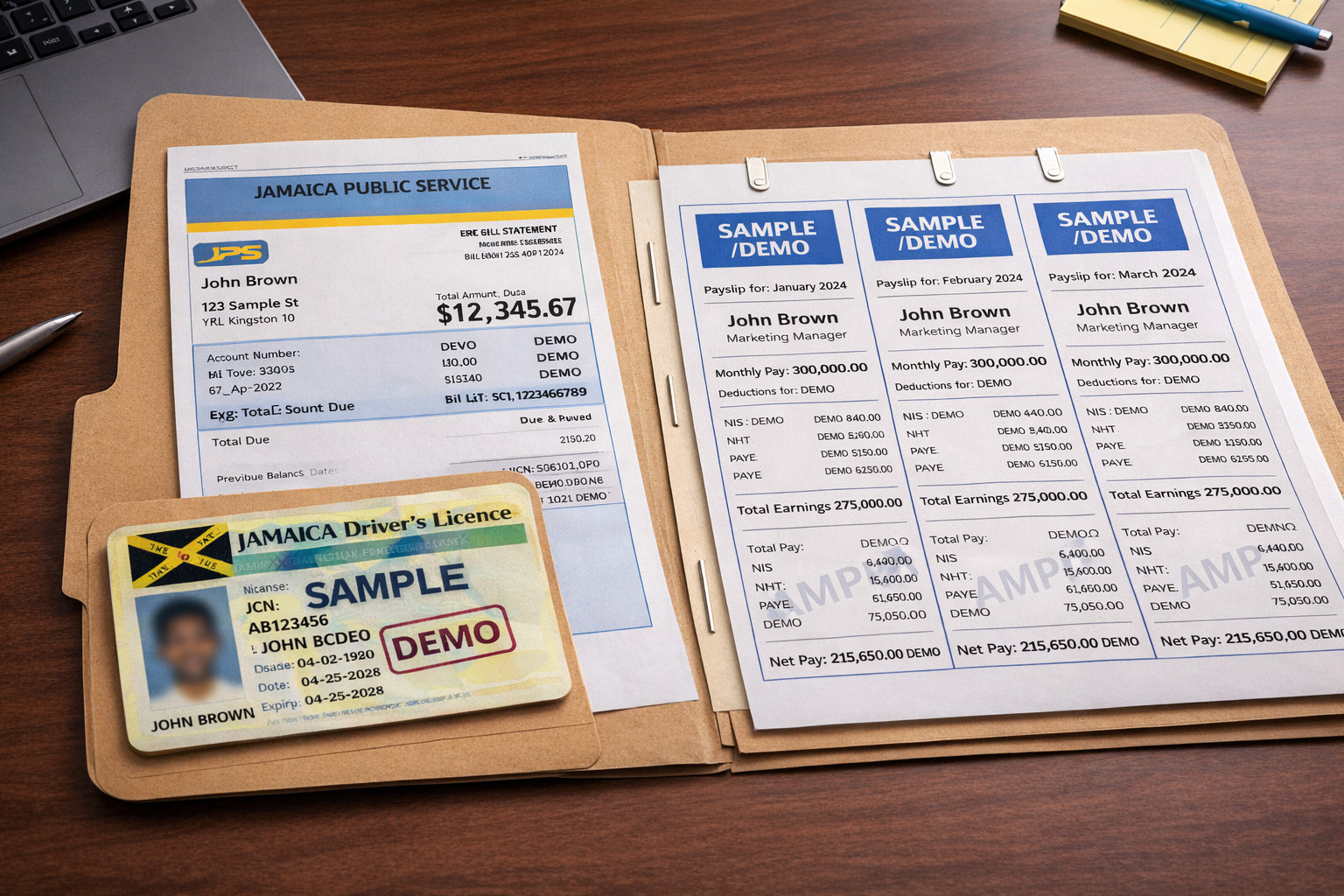

Banks must confirm who you are to prevent fraud. This can include a passport, driver’s licence, voter’s ID, or TRN. Without proper ID, someone could pretend to be another person and borrow money illegally.

Proof of Address

Documents like a utility bill or a bank statement show where you live. This helps the lender confirm stability and know how to contact you if needed.

Proof of Income

Banks need evidence that you earn money regularly.

If someone is employed, they may submit a job letter, payslips, or bank statements.

If self-employed, they might provide business documents, tax records, or financial statements.

Proof of Assets

For some loans, borrowers may show ownership of assets like a car or property. These can help reduce risk for the lender. They can be used as collateral.

Details of Existing Debt

Loan or credit card statements help lenders understand how much the borrower already owes.

So why are these documents necessary? Banks are lending real money that must be paid back. Supporting documents help them check three things:

- Is the borrower genuine?

- Do they have stable income?

- Can they realistically repay the loan?

In short, supporting documents protect both sides — the bank from losses, and the borrower from taking on debt they may not be able to handle.