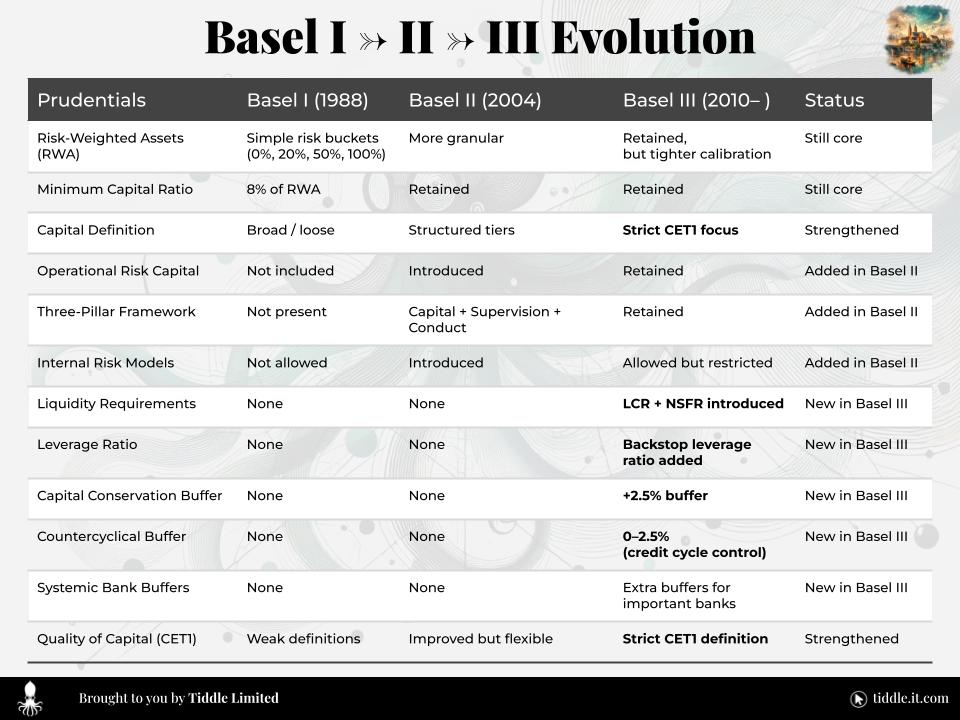

After the 2008 Global Financial Crisis, regulators saw a clear problem: many banks looked strong but were actually fragile.

They had:

- too little high-quality capital

- too much borrowing

- not enough liquidity

- funding structures that could collapse quickly

Basel III was created by the Basel Committee on Banking Supervision to fix this.

Global Adoption

Basel III is not a law. It is a global standard adopted by countries through their own regulators.

Today, most major jurisdictions—including the US, UK, EU, and many developing economies—apply Basel III–aligned rules, sometimes with local adjustments.

1. Capital — A Real Safety Cushion

Banks must hold strong, loss-absorbing capital.

Common Equity Tier 1 (CET1) Ratio:

CET1 Ratio = CET 1 Capital ÷ Risk-Weighted Assets

- Common Equity Tier 1 Capital: the bank’s own money—shares and retained earnings that absorb losses

- Risk-Weighted Assets: loans and investments adjusted based on how risky they are

Minimum:

- 4.5% + 2.5% buffer = 7%

This means: for every $100 of risk, the bank should have at least $7 of real capital.

2. Leverage — Limiting Excess Debt

Banks cannot rely too heavily on borrowed money.

Leverage Ratio:

Leverage Ratio = Tier 1 Capital ÷ Total Exposure

- Tier 1 Capital: core capital that can absorb losses (including common equity)

- Total Exposure: everything the bank is exposed to—loans, assets, and commitments—without adjusting for risk

Minimum:

- 3%

This means: for every $100 of total exposure, the bank should have at least $3 of capital.

3. Liquidity — Surviving Short-Term Stress

Banks must hold assets they can quickly convert to cash.

Liquidity Coverage Ratio (LCR):

LCR = HQLA ÷ 30-day Net Cash Outflows

- High Quality Liquid Assets (HQLA): cash or assets that can be quickly sold without losing value

- 30-day Net Cash Outflows: the cash the bank would likely need over 30 days in a crisis

Requirement:

- ≥ 100%

This means: the bank must have enough liquid assets to survive a month of stress.

4. Stable Funding — Long-Term Discipline

Banks must fund long-term assets with stable sources.

Net Stable Funding Ratio (NSFR):

NSFR = ASF ÷ RSF

- Available Stable Funding (ASF): reliable funding like equity and long-term deposits

- Required Stable Funding (RSF): the amount of stable funding needed based on the bank’s assets

Requirement:

- ≥ 100%

This means: stable funding must fully cover the bank’s long-term needs.

5. Capital Buffers — Preparing for the Cycle

Basel III adds extra protection tied to the credit cycle:

- Capital Conservation Buffer (2.5%)

- Countercyclical Buffer (0–2.5%)

These force banks to build capital in good times and use it in bad times.

Final Insight

Basel III is not just a set of formulas.

It is a system designed to control the credit cycle—to prevent banks from over-lending during booms and collapsing during downturns.

In simple terms:

Basel III exists to make banks strong enough to survive stress and stable enough not to cause it.